Tokenization of Real-World Assets: A Comprehensive Guide

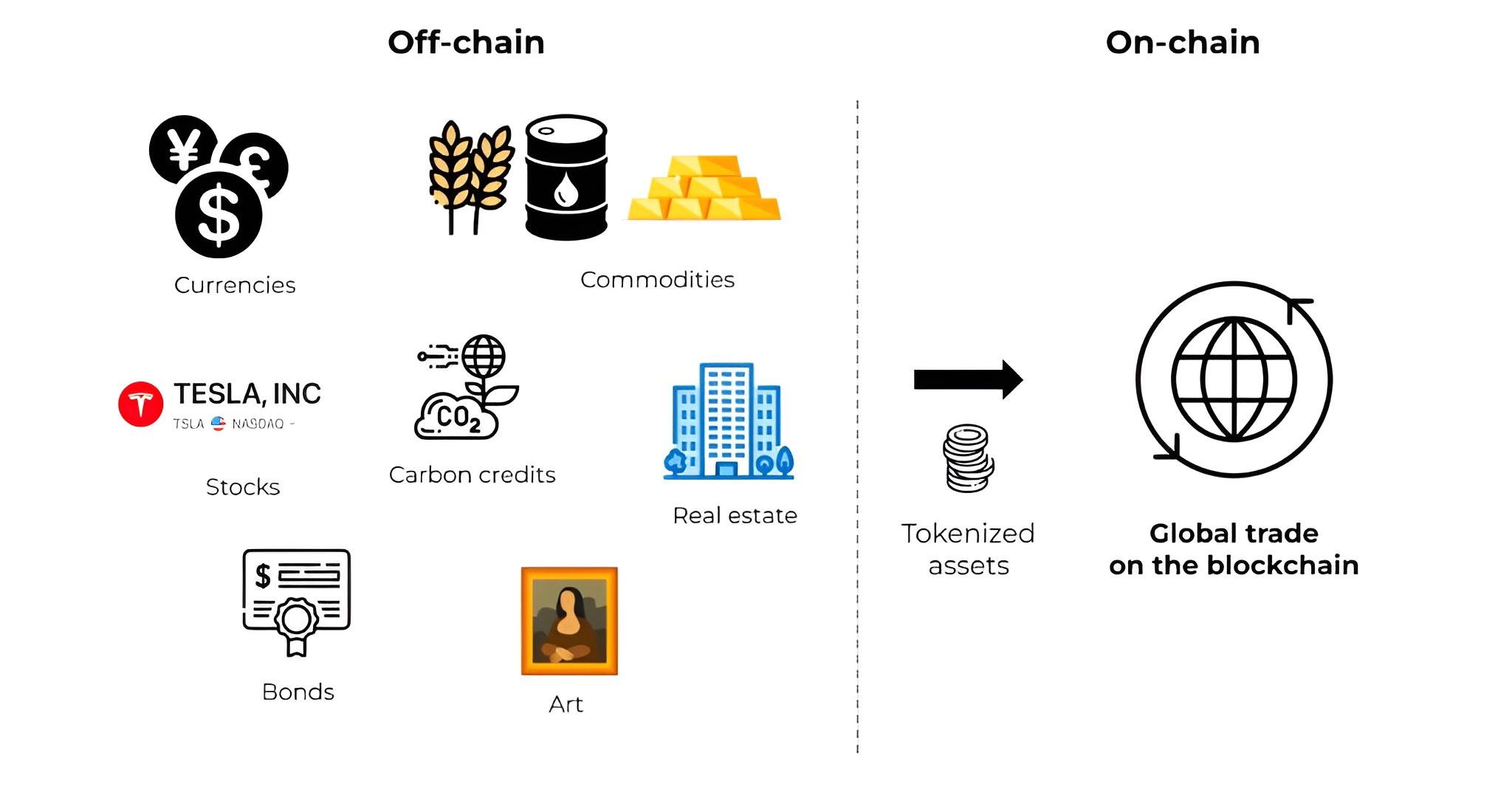

The thrilling advance of digital technology is reinventing how people can engage with assets, bringing the esoteric world of tokenization into the mainstream. In uncomplicated terms, tokenization turns the rights to assets into digital tokens that are recorded on a blockchain - much like a cryptographically secured digital diary that everyone can trust. This allows for the buying, selling, and holding of digital versions of real-world assets (RWA), such as property, art, and investment interests.

Understanding Tokenization and Its Opportunities

The tokenization revolution has rolled in to offer tangible benefits. Imagine transforming an otherwise illiquid asset, like a masterpiece of art or a swath of real estate, into something you could trade any day of the week across the globe. Tokenization makes this possible by slicing high-value items into smaller parts, opening the door for retail investors to own just a fraction of what once seemed unattainable.

At its core, tokenization represents a quantum leap in asset management. Blockchain technology functions as a transparent, secure online ledger that tracks and facilitates trading in digital formats of real-world assets – from real estate to artworks and financial securities. This innovation promises enhanced operational efficiency, faster settlements, and access to a broader investor base.

The data speaks volumes about the rapid pace of adoption, as the market for tokenized RWAs experienced a whopping 308% growth over three years, reaching $24 billion today with projections aiming as high as $30 trillion by 2034. Clearly, there is a massive shift underway as institutions leverage blockchain's infrastructure for tangible gains.

The Role of Blockchain Technology

Blockchain technology sits at the heart of this transformation, functioning as an open ledger that no one party can control. It heralds unprecedented transparency, ensuring that every transaction is visible and trustworthy. Smart contracts on blockchain platforms automate actions based on predefined conditions, streamlining trading and settlement without the typical delays or middlemen.

Tokenization simplifies complex concepts. If the physical world uses items like casino chips and concert tickets to symbolize financial rights or privileges, the digital realm applies the same concept to tokens. These digital assets, rooted in distributed ledger technology, can represent ownership or value, either created specifically for the blockchain (native tokens) or linked to real-world objects (linked tokens).

Smart contracts, which are essentially self-executing agreements coded into the blockchain, manage everything from issuance to compliance and transfers, ensuring a transparent and automated process. This allows RWAs to be divided and traded with unprecedented ease while leaving a verifiable audit trail to ensure transparency.

Mainstream Adoption by Financial Institutions

There has been a fascinating shift from tokenization being a niche practice within fintech startups to a transformative trend adopted by leading financial institutions. Tokenization now supports the custody and settlement services offered by mainstream entities, while traditional asset managers explore the benefits of tokenized share classes on global exchanges like never before.

The pioneering efforts in tokenizing fund products illustrate the disruptive potential of this technology within the financial world. Across regions, from the UK's regulatory blueprints to the European Union's DLT Pilot Regime, frameworks are being laid to harmonize tokenized asset trading and embolden cross-border liquidity.

Tokens can be created for nearly any object of recognized value, be it real estate, intellectual properties, or even fine art. By breaking down high-value assets into smaller units, ordinary investors gain the opportunity to own goods that would otherwise remain beyond their reach.

Legal and Regulatory Considerations

As tokenization matures, a myriad of nuanced regulatory challenges come to the forefront, demanding that financial service providers and advisors pay close attention. The distinction between "on-chain", "off-chain", and "hybrid" tokens presents unique implications for asset ownership and legal enforceability. While "on-chain" tokens offer a complete digital record on a distributed ledger, making ownership transparent and verifiable, "off-chain" tokens still rely on traditional legal frameworks.

An exciting aspect is the hybrid model – where legal information on tokens remains on the blockchain ('on-chain'), while sensitive data stays with traditional custodians ('off-chain'). This model allows capturing the efficiency of digital ledgers while adhering to established legal standards for things like dispute resolution and privacy.

Understanding whether a token serves as an informational, certificatory, or dispositive tool is crucial, as this dictates the enforceability and protection of an investor's rights. In an era where transparency and proof of ownership are paramount, these distinctions become critical.

On the regulatory front, there are significant challenges regarding cross-border compliance, security risks, and the application of current financial market regulations to digital assets. Jurisdictions like the UK treat tokenized assets akin to traditional securities, applying established financial regulation and anti-money laundering laws to this innovative technology.

Benefits: Liquidity, Efficiency, and Transparency

The tokenization of assets introduces a game-changing level of liquidity. Historically, certain assets like real estate or art were out of reach for many investors due to high cost barriers and low tradability. With tokenization, these assets can now be divided into smaller, fractional interests, enabling a wider range of investors to participate and drastically lowering the financial threshold to ownership.

Efficiency in the trading and management of assets becomes significantly heightened through Distributed Ledger Technology. By utilizing smart contracts, tokenization allows for automated, instantaneous execution of agreements. This reduces the reliance on intermediaries, streamlining the process and cutting down on delays and costs associated with manual settlements.

The transparent nature of blockchain technology sets a new standard for accountability and security in financial transactions. Distributed ledgers can be verified by anyone with access, mitigating the risk of fraud and ensuring compliance with regulations. The utilization of smart contracts further reinforces this transparency by automating governance protocols and regulatory requirements.

Challenges and Risks

Yet, as with all innovations, tokenization presents its share of hurdles. Navigating the regulatory environment is crucial, particularly where traditional and digital domains intersect. The use of tokenized fund units as "security tokens" under financial regulation is a process that existing legal frameworks are just starting to accommodate.

A significant puzzle lies in ownership and title transfer. The digital versus physical custody conundrum persists, with uncertainty over the legalities of transferring tokenized units. When does digital ownership become legally binding? And what happens if a dispute arises? The nascent nature of legal recognition for blockchain-recorded ownership adds complexity to token management.

Smart contracts must include all traditional legal contract elements to be enforceable. While revolutionary in automating processes like issuance and distribution, they must navigate legality hurdles where century-old principles meet new-age technology.

The digital world also brings security risks. Issues such as private-key theft and protocol bugs hold tokenization's growth potential at bay. Blockchains' immutability means mistakes can become permanent, raising the stakes for security and privacy measures more than ever.

A Path Forward

In the broader picture, tokenization is not just a financial fad; it's a new way to think about ownership and trade in the digital age. With mainstream institutions climbing aboard, the future looks promising for those ready to merge established practices with digital innovation, heralding a new era of financial inclusivity and efficiency.

The rising tide of tokenization holds exciting potential for revolutionizing the finance industry by increasing asset liquidity, improving operational efficiency, and enhancing transparency. These benefits make tokenization an attractive proposition, not only for established financial institutions but also for everyday investors eager to participate in previously inaccessible markets.

While the potential of fund tokenization is vast and exciting, with its ability to lower investment barriers and increase liquidity, the challenges are serious. Navigating these risks will require robust legal frameworks and innovative solutions to yield the immense benefits promised by tokenization in our evolving digital marketplace.

{kind=link}